Demand for dry van capacity on the spot truckload market gained steam during the week ending June 22 as jurisdictions ease shopping restrictions and retailers ship goods ahead of the Fourth of July holiday and close of Q2.

After slowing the previous week, the number of posted loads increased 15.6% and spot van and refrigerated rates recovered their momentum, saidDAT Solutions, which operates the industry’s largest load board network.

The number of available trucks on the DAT network dipped 3.5% week over week. National average spot van and reefer line-haul rates, which exclude a fuel price adjustment, were higher than where they were before the coronavirus crisis started in February.

National monthly average spot rates through June 22:

- Van: $1.76 per mile, 16 cents higher than the May average

- Flatbed: $2.04 per mile, 14 cents higher than May

- Reefer: $2.11 per mile, 9 cents higher than May

Those are rolling averages for the month and current rates are trending higher. On June 1, the van spot rate averaged $1.72 a mile, the flatbed rate was $1.98, and the reefer rate was $2.08.

Trendlines

Vans near year-ago levels: After the massive spike in load posts in early March when the pandemic shutdown took hold in the U.S., load posts have returned to season norms and now track closely with 2019 levels. At 3.6 loads per truck, the national average van load-to-truck ratio is ahead of the June 2019 average.

Average rates fell on just 11 of DAT’s top 100 van lanes by volume last week. The biggest drop was on the lane from New Orleans to Dallas, where prices had previously spiked due to Tropical Storm Cristobal. Rates were back down 15 cents to $1.68 per mile last week.

Retail markets make gains: Load-to-truck ratios have soared in Memphis, a major market for retail warehousing. Spot van prices rose on several lanes out of Memphis:

- Memphis to Atlanta rose 16 cents to an average of $2.40 per mile

- Memphis to Indianapolis was up 20 cents to $2.23 a mile

- Memphis to Columbus rose 19 cents to $2.14 a mile

Reefers rise seasonally: The national average reefer load-to-truck ratio jumped to 5.4 loads for every truck posted to the DAT network, up from 4.3 the previous week. Volumes were steady as more shipments of domestic produce balance out a reduction in imports from Mexico, Canada, and other markets.

Watermelon and berry seasons are driving up volumes in Florida and southern Georgia, while out West the cherry season in Stockton, Calif., is drawing to a close and shifting to Washington state. According to the Northwest Cherry Growers, the Pacific Northwest cherry season expects to produce close to 20 million 20-pound boxes, which equates to around 625 truckloads per week over the 16-week season ending late August. The Pacific Northwest should provide plenty of opportunities for carriers looking for loads out of Washington and Oregon through the end of July.

COVID-19 trends to watch

- COVID cases in agricultural markets: New COVID-19 cases are hitting Texas, Georgia, South Carolina, Arizona, California, and other states where the weather is hot and agricultural production is in full force.

- Early peak for reefer rates: The usual mid-July seasonal reefer rate spike will be lower this summer as restaurants and food services industries grapple with reopening and summer travel takes on a very different look.

- Port volumes: Lower volumes at major U.S. ports are affecting both the coastal dray and truckload dry van markets. The Port of Los Angeles reported close to 30% fewer containers moved in May compared to the same time last year. Imports dropped 28.4%, while exports were down 37.6%. On the opposite coast at the nation’s number-two port, Elizabeth, N.J, container volumes dropped 7.5% in May year over year.

Photo: DAT Solutions

Photo: DAT Solutions

After a trying 2019, COVID-19 created even more challenges for the trucking industry in 2020. The pandemic created a hectic spring that saw sharp demands spurred by stay-at-home orders and panic buying that was contrasted by withering demand from closed businesses. Plus, a looming recession has created market uncertainties.

Motor carriers who don't adapt to the new normal of this COVID-19 world might not make it to the other side, according to the Council of Supply Chain Management Professionals (CSCMP) 2020 State of Logistics Report, which was released on June 23. But those carriers who do adapt and find a way to survive the uncertainties of 2020 could find themselves in a good position — with less competition — once the U.S. emerges from the pandemic.

At the start of this year, “Consumer confidence seemed to be picking up after reaching lower levels in 2019 when compared to 2018 — we know what happened next,” said Michael Zimmerman, a partner with Kearney, and co-author of the report.

The report, released annually for the past 31 years, offers a snapshot of the U.S. economy from the logistics sector’s view of the overall supply chain. It is a compilation of leading logistics intelligence from around the world, combined with industry trends, to offer insights on the modern industry supply chains.

“2019 was a strong year for logistics activity, and the numbers we saw at the beginning of 2020 seemed to be our way of welcoming the new decade. To say that everything changed is an understatement,” noted Rick Blasgen, president and CEO of CSCMP. “Supply chain management professionals deal with change daily, and many in our industry have led efforts in adapting, innovating, and managing through unprecedented disruption while simultaneously creating new operating models.”

Blasgen noted that the logistics report offers a historical snapshot and look into the future. Even if that future is uncertain, the main theme of the report is that both carriers and shippers need to adapt.

Co-author Zimmerman, who spoke with industry media in advance of the annual CSCMP report’s release, noted that logistics leaders are now hoping for recovery that could take on various forms. Whether that economic recovery is shaped like a “V,” an “L” or a “swoosh, we know that the bulk of the logistics in the U.S. — where consumption is some 70% of GDP — is going to have to adapt. That means further cutbacks by carriers and a rise in bankruptcies, at least in the short term.”

In the first half of 2019, 640 motor carriers went out of business, citing falling rates and demand, increased tariffs and trade tensions, increased insurance costs, and rising driver pay. The report notes that the failures of the first half of 2019 more than doubled the number of trucking companies that went out of business in 2018.

This is a trend that is likely to continue during the COVID-19 pandemic, the authors argue. "Thus, as a carrier, you're justified in putting all your chips on short-term survival," according to the report. "If you can make it through the next six to 18 months, other carriers will drop out, capacity will tighten, rates will rise, and your longer-term outlook will be more stable."

GDP forecasts for the rest of 2020 and 2021 are being revised downward as supply chains are navigating an extraordinary landscape in the U.S. and abroad. Before COVID-19 changed that landscape, modern supply chains were lauded for their ultra-efficient, single-source and just-in-time capabilities. Now, the report notes that the logistics field will need to construct entirely new levels of supply chain resilience.

In this COVID-19 world, Zimmerman said, shippers are going to have work harder with carriers to diversify routing. This comes after scarce capacity and increasing rates in 2019 tipped the market balance in favor of shippers, according to the report. This led to lower rates for carriers and profitability concerns last year.

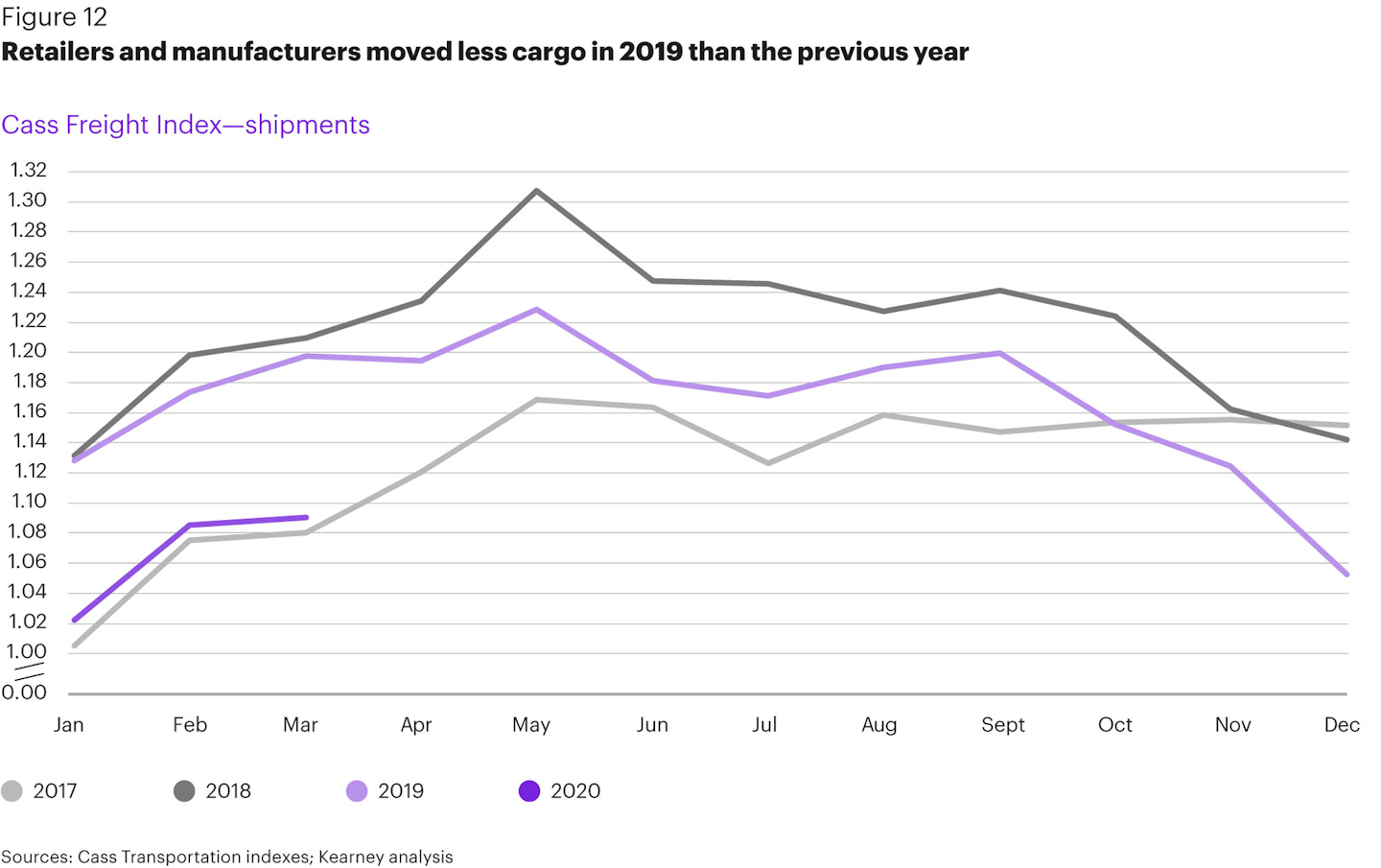

Freight rates dipped year-over-year for six months straight last year: Prices on trucking’s spot market were down 22% in June 2019 compared to 2018 — and load posts dropped by 27% over the same time frame, according to Truckstop.com. The CSCMP report noted this was because demand declined while supply increased as retailers moved less cargo in 2019 than the year before, according to the Cass Freight Index.

“Now, with COVID-19 and the consumer caution it has brought — and the continued demand destruction it has wrought — road carriers will need to do something different, to survive and do better,” Zimmerman said.

He said big carriers are looking to technology investments to increase efficiency in routing and fuel consumption. Smaller carriers are relying on strong customer relationships and looking to app-based solutions and brokers to provide better route fits and backhauls.

The pandemic has created a stark contrast for trucking compared to just two years ago, according to CSCMP’s logistics report. In mid-2018, when prices were highest, load-to-truck ratio was more than 60. In 2019, that figure fell below 30. Then, in March 2020, the ratio jumped to 46 — reflecting consumer demand at groceries and pharmacies — before returning to 2019 levels in April.

While COVID-19 accelerated demands for groceries and home consumables, it slowed the demand for manufacturing and hospitality. The pandemic has also accelerated consumers’ shift from brick-and-mortar retail shopping to e-commerce, which, as CSCMP notes, means fewer warehouse-to-store deliveries and more traffic in and out of last-mile fulfillment centers.

The economic fallout of COVID-19 will affect carriers differently, depending on markets and regions, the report noted. Farm-to-grocer supply chains are expected to benefit, for example, while carriers delivering cross-border auto parts will likely struggle. There also could be regional differences depending on how the virus spreads. And smaller carriers with customers in the worst-hit industries will be hit the hardest this year, according to the report.

Here is a look at some other key report findings:

- In 2019, the national economy saw 2.3% growth, taking the U.S. economy to $21.43 trillion in GDP. The logistics industry grew to $1.652 trillion in expenditures. Its productivity improved, bringing its cost to 7.6% of GDP, an improvement from 7.9% in 2018.

- Road freight, the biggest segment of U.S. logistics spend, was slowing down in 2019 after a torrid 2018 as years of scarce capacity and increasing rates reversed in favor of shippers.

- COVID-19 has been more economically damaging than a standard recession or an escalation of trade tensions. The current pandemic-driven recession ended 126 months of growth, the longest economic expansion in U.S. history.

- The pandemic and public response accelerated an already fast-growing e-commerce industry, which has different logistics needs than traditional retailing.

- When the economic recovery begins to occur, it will likely be uneven and staggered.

- The consumer confidence index dropped 18.1 points in early April; March saw an 11.9-point decline.

The report also suggests steps the logistics industry can take build a modern, long-term supply chain:

- Support demand for surges in areas such as groceries and e-commerce.

- Reconfigure supply chains for other sectors — such as heavy industry — that have cratered.

- Adapt to the residual effects of social distancing as the industry accommodates a larger consumer desire for home deliveries.

- Redirect idle trucks and distribution center capacity to the booming sectors: Companies should recognize that logistics providers cannot reconfigure all their capabilities and relationships on the fly.

- Supply chains need to be more flexible to cope with uncertainty. That will result in less emphasis on lean operations and more on optionality and inventory.

- Will this all lead to more reshoring of manufacturing operations?

- The advancement of 5G technology will play an important role in further increasing supply chain visibility.

The 31st annual CSCMP State of Logistics Report is researched and prepared by global consulting firm Kearney and presented by Penske Logistics. It is available free for CSCMP members and available for purchase by non-members.

"load" - Google News

June 24, 2020 at 10:19PM

https://ift.tt/381M2Gr

DAT: Spot load posts increased 15% last week; truckload rates respond - Fleet Owner

"load" - Google News

https://ift.tt/2SURvcJ

https://ift.tt/3bWWEYd

Bagikan Berita Ini

0 Response to "DAT: Spot load posts increased 15% last week; truckload rates respond - Fleet Owner"

Post a Comment